Monday Morning Espresso - W21'25

Markets entered the week digesting a bout of volatility following the U.S. credit rating downgrade, coinciding with Trump’s “Big Beautiful Bill”. This was followed by the eurozone’s GDP-growth downgrade for 2025, now at 1.1%, down from 1.5% in the November forecast. Meanwhile, Bitcoin surged to new all-time highs.

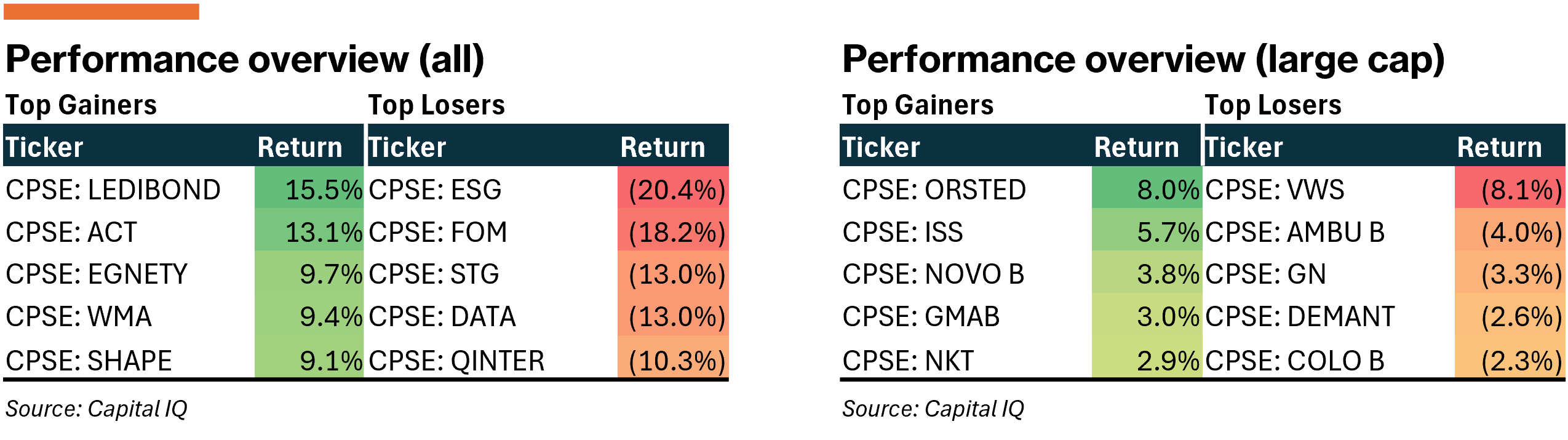

Nordic markets drifted lower, ending the week down -1.9%. Investors weighed a mix of macro data, the tail end of earnings season, and the first wave of many upcoming Capital Market Days (CMD).

Denmark

Shares in Copenhagen started the week on strong footing but gave back gains as the week progressed, with the all-share index (+1.3%) and large-cap index (+0.0%) closing the week flat. The week featured earnings from, among other, Better Collective (CPSE:BETCO DKK/OM:BETCO) — a name we've covered in depth. All things considered, we are pleased with the performance.

Building insulation provider, Rockwool (CPSE:ROCK B) delivered a solid Q1-2025, with sales of EUR 959m and adj. EBIT of EUR 154m — both ahead of consensus, driven by insulation and strong double-digit growth in North America. Eastern Europe declined 7% in LC (drag from Russia), while Western Europe remained muted. Systems margin fell 3.2pp YoY, mainly due to weaker profitability in Grodan. Cash flow was solid, yet slightly dragged by working capital build-up, but nothing material in Q1-context.

Guidance for FY2025 was reiterated: LSD sales growth in LC, ~16% EBIT margin, and EUR 450m capex. Considering the solid start to the year, management’s tone was conservative going into H2-2025. The company trades at 8.9x fwd. EV/EBITDA — a ~5% premium to its long-term average. We remain sidelined due to better opportunities elsewhere.

The Q1 earnings season in Denmark has largely come to an end, yet we will follow management’s commentary for Per Aarsleff (CPSE:PAAL B) who updated their FY2025 outlook and preannounced headline figures a few weeks ago.

Earnings review & other news

Ørsted (CPSE:ORSTED) and Vestas (CPSE:VWS) both rallied early in the week after the Trump administration lifted a work halt on Equinor’s Empire Wind project — a move that markets viewed as a positive read-across for Ørsted’s Sunrise Wind, which had faced similar regulatory risk. Yet, sentiment for Vestas (CPSE:VWS) reversed as new U.S. proposals signaled an accelerated rollback of the Inflation Reduction Act, with a potential hard stop for tax credits by end-2028 and a 60-day construction start requirement.

Scandinavian Tobacco Group (CPSE:STG) delivered a soft Q1-2025, missing on revenue (DKK 1,974m, -5% vs. cons.), adj. EBITDA (DKK 317m, -17% vs. cons.) and EBIT (DKK 136m, -36% vs. cons.). The miss was tied to SAP-related supply issues and softer U.S. demand. FY2025 guidance was cut: sales now DKK 9.1–9.5bn (prev. 9.2–9.7bn), EBITDA margin 18–22% (prev. 20–23%). While FX and tariffs drove the downgrade, investor confidence remains fragile after now having four consecutive years of guidance misses.

Matas (CPSE:MATAS) delivered a mixed Q4-2024/25, missing on revenue (DKK 1,878m vs. cons. DKK 1,902m) and adj. EBITDA (DKK 216m vs. cons. DKK 243m). The softer performance was owing to weaker performance at KICKS and a more uncertain consumer sentiment. On the positive side, online sales grew +24% ex-SkinCity, cost synergies from KICKS were raised by DKK 50m (total now DKK 190m by FY27), and capital returns were stepped up with a DKK 100m buyback and new ≥40% payout policy. FY2025/26 guidance is 3–7% organic topline growth alongside ~15% EBITDA margin — the midpoint being ~5% below consensus.

Nykredit received all regulatory approvals to proceed with its DKK 24.7bn acquisition of Spar Nord Bank (CPSE:SPNO) at DKK 210.50/share. Nykredit will delist the bank and launch a compulsory buyout of remaining shares. The deal will create Denmark’s third-largest bank with combined lending of ~DKK 160bn.

BlackRock has increased its stake in GN Store Nord (CPSE:GN), crossing the 5% ownership threshold. The company has been the subject to takeover speculation following a ~85% share price collapse since mid-2021, with William Demant Invest (~10% stake and owner of peer, Demant (CPSE:DEMANT)) and several PE funds reportedly circling the name.

Sweden

In Stockholm, sentiment was mostly negative driven by Industrials — yet, offset by Consumer Staples and Telecom. Notably, the week featured the dual-listing of Icelandic biotech company, Alvotech (OM:ALVO SDB). The all-share index (-3.1%) and large-cap index (-2.5%) both gave back gains.

On a more constructive note, Swedish construction starts rose +0.3% in April, with residential activity up +1.4% — supported by improving financing conditions. With market expectations leaning toward further rate cuts in 2025, companies like FasadGruppen (OM:FG), Instalco (OM:INSTAL), and Byggmax (OM:BMAX) should be well positioned to capitalize on a demand-recovery.

BioArctic (OM:BIOA B) delivered Q1-2025 net revenue of SEK 1,290m (SEK 1,294m cons.) and operating profit of SEK 1,075m (SEK 1,044m cons.), bolstered by a USD 100m upfront from Bristol Myers Squibb and a EUR 10m milestone from Eisai. Royalty income rose nearly 5x YoY to SEK 96m, while operating expenses doubled to SEK 201m, primarily due to FX effects. Cash flow from operations turned positive at SEK 11.8m, though working capital drag (notably SEK -1,007m in receivables) weighed on cash conversion.

Guidance from partner Eisai implies Leqembi sales of SEK ~5.1bn, slightly below consensus and thus weighing on royalty revenues. Going into the report, consensus had estimated royalty revenue of SEK ~550m; a figure that will likely be revised downward in due course.

Management has communicated the potential for dividend distributions as early as next year, contingent on earnings consistency. Despite early optimism in the wake of the report, shares sold off after Eli Lilly’s donanemab gained approval in Australia — where BioArctic’s lecanemab was previously rejected.

The coming week will feature CMD from SAAB and Sivers Semiconductors, as well as the last tail of earnings reports from the likes of Ekta (OM:EKTA B), CodeMill (OM:CDMIL), Acroud (OM:ACROUD), among other.

Earnings review & other news

Asmodee (OM:ASMDEE B) posted Q1-2025 organic sales growth of 23.6% to EUR 341m (cons. EUR 289m), driven by strong momentum in partner-published games (+32.5%) and own-published titles (+10.2%). Adj. EBITDA margin landed at 11.9% (cons. 11.2%), pressured by mix and elevated OPEX. Free cash flow (incl. tax and leases) reached EUR 95.1m. The company is reviewing its supply chain (12% of U.S. sales sourced from China) and introducing price increases and cost controls amid U.S. tariff risks.

Embracer (OM:EMBRAC B) reported Q4-2024/25 organic sales growth of 19% to SEK 5,386m (cons. SEK 5,427m), down from SEK 5,757m LY. Adj. EBIT came in at SEK 1,077m (cons. SEK 937m; SEK 1,046m LY). Shares fell sharply on weak FY2025/26 guidance: Sales slightly higher YoY, with EBITDA and adj. EBIT kept flat. The outlook implies ~5% and ~26% downside vs. consensus on revenue and EBIT, respectively — reportedly tied to a major title delay (likely Metro) into FY2026/27.

The Persson family, via Ramsbury Invest, acquired an additional 3m shares for SEK 435m in H&M (OM:HM B). The family now controls 63.7% of share capital and 82.6% of voting rights.

IK Partners has fully exited Netel (OM:NETEL), selling its 46.7% stake for SEK 192m at SEK 8.50/share — implying an EV of EUR 112m and an EV/adj. EBITA (Q1-2025 LTM) of 7.8x. Buyers included Etemad Group, CEO Jeanette Reuterskiöld, and CFO Fredrik Helenius. Netel reported Q1-2025 LTM revenue of SEK 3,302m and adjusted EBITA of SEK 170m.

Finland

Helsinki’s 11-day green streak broke midweek, with losses in Industrials and Telecom weighing on indices. Both the all-share index (-0.8%) and large-cap index (-0.6%) drifted slightly lower. A notable development came from newly-listed GRK Infra (HLSE:GRK), which disclosed that its subsidiary is under regulatory scrutiny for anti-competitive practices in the asphalt market.

Konecranes (HLSE:KCR) hosted its CMD with few surprises but strong signals of execution. Group EBITA margin target was raised to 13–16% (prev. 12–15%), to be reached by 2029. Services remains the key long-term value driver, with management presenting a credible strategy to expand its high-margin agreements through digitalization, predictive maintenance, and increased outsourcing from customers.

U.S. demand commentary was strikingly resilient — no tariff impact, pricing is sticking, and activity remains stable into Q2-2025. This supports near-term confidence across segments, with read-through to Kalmar (HLSE:KALMAR) and Hiab (HLSE:HIAB). Capital allocation remains conservative, prioritizing capex and dividends ahead of M&A and buybacks. With NIBD/EBITDA at 0.2x and 2025E EV/EBITDA at ~7x (cons.), we would have welcomed a more forward-leaning stance on buybacks.

While the earnings season is largely complete in Finland, the week ahead will offer CMDs from Orion (HLSE:ORNBV), Raisio (HLSE:RAIVV), and Inderes (HLSE:INDERES).

Earnings review & other news

Stora Enso (HLSE:STERV) announced the sale of ~175,000 hectares of Swedish forest assets (~12.4% of local holdings) for EUR 900m. Buyers include Soya Group (40.6%) and a MEAG-led consortium (44.4%), with Stora Enso retaining 15%. The deal is expected to reduce net debt by EUR 790m and supports the shift toward packaging and biomaterials. Closing is expected during Q3-2025 — subject to regulatory approval.

Fondia (HLSE:FONDIA) appointed co-founder Timo Lappi as permanent CEO, effective May 19, after serving as interim since January. The company also updated its medium-term targets: organic revenue growth and adj. EBITDA margin to sum to ≥20% (prev. ~15% growth and 15% EBIT margin).

Wetteri (HLSE:WETTERI) reported Q1-2025 revenue of EUR 115.5m (vs. cons. EUR 126m) and an adj. operating loss of EUR -1.4m (vs. cons. EUR +2.0m), with EPS unchanged YoY at EUR -0.02. On May 14, the company withdrew FY guidance citing early-year underperformance and rising uncertainty in the Nordic auto market. Management flagged tentative orderbook stabilization — but visibility remains low at this point.

Musti Group (HLSE:MUSTI) reported Q1 2025 revenue of EUR 119.8m (vs. EUR 107.2m LY), while margins compressed with adj. EBITDA at EUR 12.7m (vs. EUR 15.0m LY), driven by elevated campaign spend. No formal guidance, though management expects EBITDA to improve as demand normalizes and Pet City integration advances.

The Finnish NYSE-listed, Amer Sports (NYSE:AS), posted a strong Q1-2025, with revenue up +23.5% YoY to USD 1.18bn (vs. cons. USD 1.14bn), adj. gross margin at 58.0% (vs. cons. 56.8%), and EBIT at 15.8% (vs. cons. 11.6%). Adj. EPS was USD 0.27 (vs. cons. USD 0.16). All three segments — Technical Apparel, Outdoor Performance, and Ball & Racquet Sports — exceeded expectations, led by Arc’teryx and Salomon. FY2025 guidance was raised: revenue growth of +15–17% (prev. +13–15%; cons. +14.4%) and adj. EPS of USD 0.67–0.72 (prev. USD 0.64–0.69; cons. USD 0.68).

Norway

Norwegian equities ended the week lower, with the all-share index(-1.1%) and the large-cap index (-0.8%) pressured by falling oil prices amid renewed speculation around OPEC+ production hikes and a series of underwhelming earnings prints.

Notably, companies tied to shipping tycoon John Fredriksen dominated headlines — incl. flagging >15% ownership in Mowi (OB:MOWI), increasing his stake in Edda Wind (OB:EWIND) following the recent takeover bid, the Q1-2025 earnings release from Frontline (OB:FRO), and more.

SalMar (OB:SALM) reported Q1-2025 operational EBIT of NOK 798m (~20% below consensus), largely due to weak performance in Central Norway. The miss was driven by a high share of downgraded fish linked to winter wounds and residual jellyfish impacts, leading to lower average weights and depressed price realisation. EBIT/kg in Norway fell 13.2% YoY. In contrast, Northern Norway delivered as expected, with strong biological conditions and slightly lower costs QoQ.

Biomass growth remains a key tailwind. Norwegian biomass is up 26% YoY, significantly outpacing industry, driven by both fish count and weight. FY2025 volume guidance was reiterated at 256kt (+20% YoY), with growth heavily weighted to H2.

Net debt rose to NOK 22bn (NOK +3.5bn QoQ), driven by a NOK 2.1bn tax payment (part prepaying resource rent) and NOK 1.4bn in biomass-linked working capital. NIBD/EBITDA now stands at 3.2x. The company trades at ~11.5x fwd. EV/EBITDA — modestly above historical levels — implying a strong H2-2025 rebound. We await cleaner figures before revisiting the setup.

In the week to come, earnings from Vow (OB:VOW), Hav Group (OB:HAV), Grieg Seafood, among other, will hit the market. Similarly, the week will feature CMDs from both Odfjell (OB:ODFB) and Orkla (OB:ORK).

Earnings review & other news

Golden Ocean (OB:GOGL) will merge with Cmb.tech in an all-share deal, following Cmb.tech’s recent NOK ~13bn acquisition of John Fredriksen’s stake. We flagged this as a likely outcome in week 13. The ownership will be split 70/30 in favour of Cmb.tech shareholders. Golden Ocean will delist from Nasdaq and Oslo Børs, while Cmb.tech seeks a secondary Oslo listing.

A.P. Møller Maritime has acquired a 25% stake in DOF Group (OB:DOFG) via a structured share distribution from Maersk Supply Service Holding (MSSH), which received the stake as payment for the sale of Maersk Supply Service to DOF in H2-2025. DOF reported Q1-2025 LTM revenue of USD 1,611m and EBITDA of USD 572m.

Geveran Trading, controlled by John Fredriksen, acquired 75,000 shares in Mowi (OB:MOWI), increasing its stake to ~77.6m shares or 15% of the company. Geveran remains Mowi’s largest shareholder.

Bakkafrost (OB:BAKKA) reported Q1-2025 revenue of DKK 2,203m (vs. cons. DKK 2,225m) and adj. EBIT of DKK 505m (vs. cons. DKK 486m; DKK 710m LY). Adj. EBITDA was DKK 694m (vs. cons. DKK 680m). Despite a pre-tax loss of DKK 36.5m (vs. profit of DKK 482m LY) due to a DKK 376m biomass write-down, operational metrics came in above consensus. The decline vs. LY was primarily driven by >18% lower salmon prices on increased supply, particularly from Norway.

MPC Container Ships (OB:MPCC) posted Q1-2025 revenue of USD 127.1m (USD 147.5m LY) and adj. EBITDA of USD 66.2m (USD 96.3m LY). Adj. EPS landed at USD 0.11/share (USD 0.17 LY) and FY2025 guidance was reaffirmed: revenue of USD 485–500m and EBITDA of USD 305–325m. Despite solid charter coverage (96% for 2025) and ongoing fleet renewal, shares fell sharply as the company cut its dividend payout ratio to 30–50% of net profit (from 75%).

Frontline (OB:FRO) reported Q1-2025 revenue of USD 428m (vs. USD 578m LY), with operational EBIT of USD 93m (vs. USD 251m LY) and pre-tax profit of USD 35m (vs. USD 180m LY). EPS came in at USD 0.15 (vs. cons. adj. EPS of USD 0.20), mainly impacted by soft product tanker markets. Dividend was set at USD 0.18/share, in line with adjusted EPS and market expectations. Management highlighted strong booking momentum heading into Q2, with VLCC rates above USD 55k/day.