Better Collective (BETCO): A Synthetic Annuity with Embedded Growth

TLDR: Better Collective (BETCO) is a founder-led, capital-light digital media platform that earns a royalty-like stream on global sports betting activity. At its core, the company directs high quality-/intent traffic to sportsbooks and, inter alia, captures a share of player lifetime value via revenue-sharing agreements. We believe the current share price fails to reflect the sticky, margin-accretive, and long-duration value embedded in these agreements.

Following a -40% share price collapse triggered by temporary regulatory headwinds in Brazil, the stock trades at ~9x EV/EBITDA — despite a proven ability to deliver double-digit organic growth, ~20% normalized ROIC, and ~70% cash conversion. Crucially, nothing has changed in the underlying demand drivers; online sports betting continues to gain share globally, and Better Collective remains well-entrenched at the top of the funnel. The company recently pivoted from acquisition-led growth toward organic execution and rewired capital allocation — including cost reductions and share repurchases.

With normalized earnings power well above the current run-rate and a re-rating catalyst likely within the next 12 months, we see a compelling risk/reward opportunity to own a high-quality asset with durable economics, led by a competent and aligned management. We believe the setup offers a path to +100% returns from current levels.

01. Background

Founded by Jesper Søgaard (CEO, 16.9% stake) and Christian Kirk Rasmussen (CO-CEO1, 16.9%) in 2004, Better Collective is perhaps the closest thing Denmark has to a dorm-room startup turned global platform business. What began as a passion project — sharing tips on “beating the bookie” — quickly evolved into something more commercially astute when it became clear that the odds tend to favor the house. The strategy pivoted toward a scalable, high-margin business model: monetizing qualified leads for online sports betting (OSB) operators and effectively earning a royalty on user behavior over time. That pivot laid the foundation for what is now a structurally advantaged businesses in the digital gambling value chain. Today, Better Collective is listed in Stockholm (OM:BETCO) and Copenhagen (CPSE:BETCO), spans ~1,500 employees, and reaches ~450 million monthly visitors via its online sports media assets.

Two decades in, the founders remain perfectly aligned — both in ownership and operating roles — and are still deeply involved in the company’s operations, with a clear drive to continue compounding its potential.

(…) for Chris and me, it has always been about the 10x. So when we hit that first EUR 10,000 or EUR 100,000 revenue per a month, well, then we aim to do the 10x of that.

— Jesper Søgaard (Founder & CEO), CMD 2023

The company is headed by an entrepreneurial management who is genuinely passionate about its mission, and complemented by a highly competent board with a demonstrated track record. Notably, the company recently added Thomas Plenborg — a respected professor (think Damodaran, but in Denmark) turned experienced board member, most known in his capacity as Chairman of the Board of DSV (CPSE:DSV) — expected to bring a layer of professionalism to Better Collective’s communication with the market.

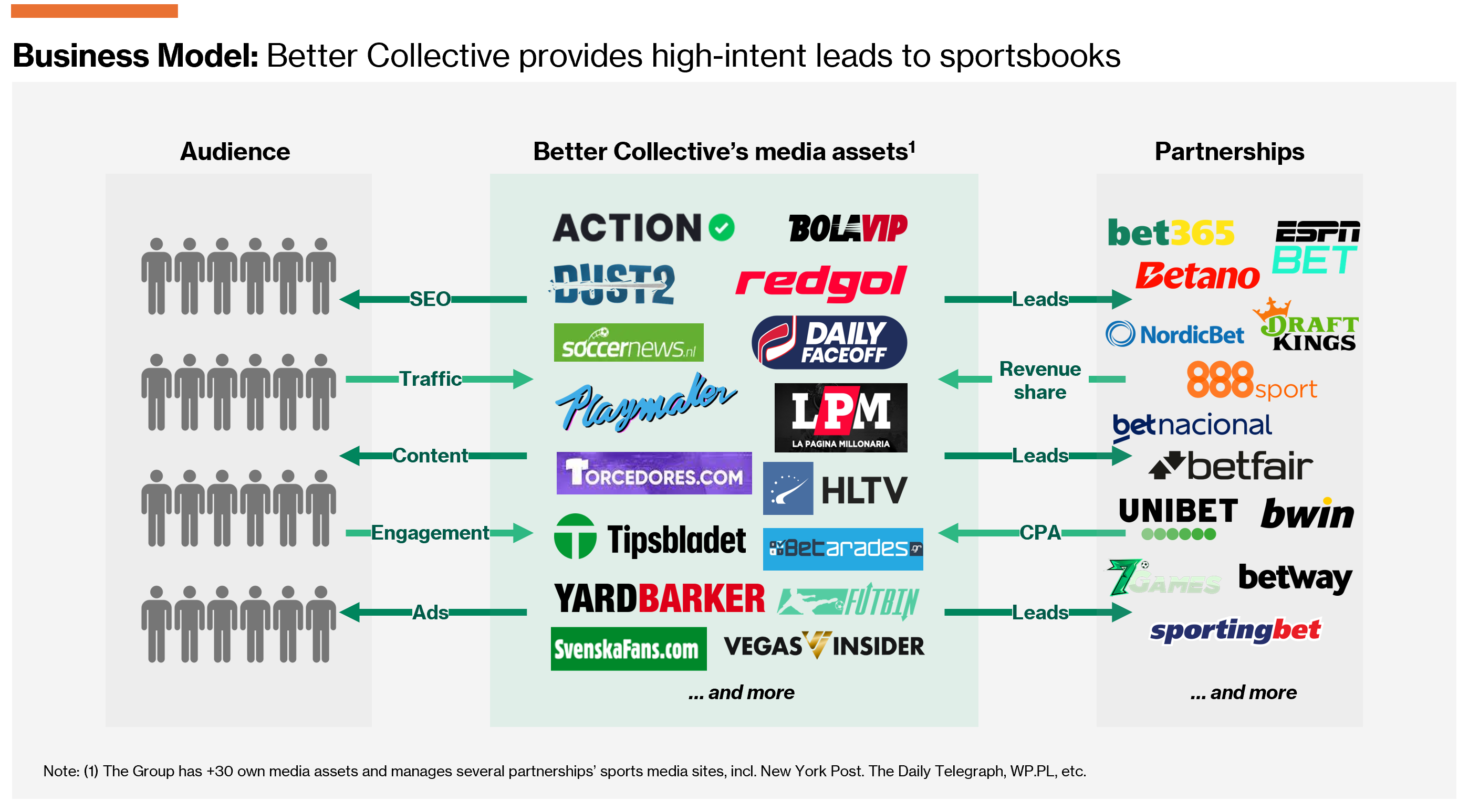

02. Business Model

The company’s core value proposition is straightforward; to deliver high-quality, high-intent leads to OSB operators (e.g., Bet365, Betano, DraftKings, etc.). This is done by capturing user attention at the top of the funnel — via its own-operated sports media sites (and media partnerships) or targeted paid advertising — and directing it to sportsbooks.

Operations are divided into two overarching segments:

(i) Publishing (71.3% of FY24A Group sales) which includes revenue from Better Collective’s proprietary sports media assets (e.g., Action Network, HLTV, VegasInsider) and media partnerships, where the audience is acquired organically — either via direct visits or SEO-optimized search results. As such, gross margins are structurally higher, as user acquisition costs are minimal and long-tail traffic compounds over time.

(ii) Paid Media (28.7%) where Better Collective acts as a performance marketing engine — acquiring traffic via paid ads (Google, Meta, etc.) and driving that traffic to its own-branded landing pages before directing said traffic to OSBs. While this strategy carries upfront customer acquisition costs (CAC), it allows for fast scaling, granular cohort targeting, and higher LTVs when coupled with revenue share agreements.

The traffic generated — whether organic or paid — is monetized through a blend of performance-based and recurring revenue streams:

Revenue Share (48.5% of FY2024A Group sales): Better Collective earns a cut of the net gaming revenue (NGR) generated by referred players over their lifetime. This creates high-margin, long-duration cash flows at no incremental costs*

CPA (24.9%): One-off fees paid by operators for each new player referred who deposits money on their platform. It offers faster cash realization but comes with less future financial upside*

Subscription (4.9%): Direct-to-consumer payments for premium content, analytics, or betting tools — primarily within Better Collective’s U.S. assets (i.e. Action Network) — delivering recurring high-margin revenues

Sponsorships (3.5%): Brand-funded content and promotional placements across Better Collective’s media properties. Essentially monetizes audience scale and engagement rather their betting behavior

CPM (2.4%)2: Traditional display advertising on Better Collective’s media properties. Typically fills unsold ad inventory and monetizes international or non-betting traffic

Other (15.7%): A mixed bucket including rent from subleases, sale of merchandise, and one-off B2B deals.

*Agreements may also be structured as Hybrid (e.g., containing both a CPA component and Revenue Share component).

03. Performance & recent events

The primary purpose of the company’s IPO was to raise proceeds to fund M&A — safe to say they have executed on that mandate. Since listing its shares in 2018, Better Collective has completed 23 acquisitions, building critical mass in high-growth markets outside Europe, notably the United States and LATAM; both regions that have undergone significant regulatory changes (see section 04. Market & positioning).

The M&A-led expansion is clearly reflected in the financials, growing topline at a 40.7% CAGR during FY2019-FY2024A (pro forma CAGR ~15.6%) alongside healthy adj. EBITDA margins of 30-40%. Similarly, the company has diversified its revenue-streams across customers3, regions4, and offerings.

A material portion of Better Collective’s economics is derived from recurring revenue streams — primarily Revenue Share (~48.5% of FY2024A sales), Subscription (~4.9%), and CPM (~2.4%) — which together account for ~62% of group revenue on a run-rated basis. We are particularly constructive on the RevShare model, which rewards patience given cash flows are delayed — but margin-accretive — and compounds steadily over time with no incremental costs.

“Building a strong competitive moat at Better Collective is also very much about delayed gratification. (…) but ultimately, we have the data that supports that if we hang on a little bit more, we know that we can get that second marshmallow. But not only that, we can three, four, fivefold our potential earnings.“

— Gavin Moore (SVP Acquisition Marketing), CMD 2024

Under the RevShare model, Better Collective absorbs part of the customer acquisition costs (CAC) internally, delivering the betting customers to sportsbooks at limited upfront cost. In exchange, the company captures a pre-agreed share of the net gaming revenues (NGR) generated from said players. This aligns incentives (i.e. driving quality traffic) and creates a deeper customer relation.

The company does not disclose figures on its total active customer base, churn rates, or similar metrics. However, by examining disclosures from listed online sportsbooks such as DraftKings, FanDuel (Flutter Entertainment), BetMGM (Entain/MGM), and Caesars Sportsbook (Caesars Entertainment), we infer that the typical customer payback period ranges from ~1.5 to 3 years. Naturally, this is dependent on several variables, incl. ARPU, the gaming tax environment, customer acquisition path (e.g., promotional versus organic), and so forth. Nonetheless, it provides a useful framework for estimating the value of Better Collectives expected RevShare contribution going forward. As for the first-year NDC shake-out (~75% churn), it is important to recognize that this includes all referred players, including low-quality, single-use participants5.

While we acknowledge the contraction in EBITDA margins since FY2019A, we view the drivers as well understood and not a cause for concern. The step-down primarily reflects two factors:

There has been a deliberate mix-shift toward Paid Media as of 2020. Given the nature of the Paid Media segment, inner-year unit economics are low but are more than offset by subsequent years’ RevShare contribution6.

The company's entry into the U.S. market and the strategic decision to shift from CPA agreements to RevShare agreements. We regard this transition as positive, as it should enhance the long-term quality and predictability of earnings.

In other words, the underlying drivers are strategic in nature and consistent with management’s efforts to optimize for durable, compounding value rather than near-term margin preservation.

Having said that, we do believe there is untapped upside in the margins at current levels — not only because margin-accretive RevShare will lift profitability — but also because the company’s busy M&A strategy inevitably introduces organizational bloat which suppresses the underlying margin potential. As such, we welcome the company’s recent pivot toward organic growth and right-sizing the organization7, enabling a leaner OPEX base to capture incremental operating leverage.

The pivot toward organic growth and cost discipline is a direct response to external pressures. In particular, H2-2025 proved difficult given (i) the anticipation of Brazilian regulatory changes weighed on sportsbook activity, pressuring both RevShare and NDC volumes; and (ii) reduced advertising spend by major U.S. customers suppressed CPA revenues, an effect amplified by the ongoing transition toward RevShare models. These developments ultimately led management to revise guidance downward, implement an EUR 50m efficiency program, and reconsider capital allocation.

“Since the IPO we have been very clear about the M&A strategy, (…) so it is a more recent thing for us to really consider the other options and the expected rate of return for different projects (…). I think right now — also because we have seen a significant share price decline in Better Collective — it ups the bar [e.g. IRR hurdle rate] for other ways to allocate cash flow versus buying back shares in Better Collective”

Jesper Søgaard (founder and CEO) in the HoldCo Builders Podcast

The downward revision of guidance pushed the shares off a cliff, declining by ~40% in a single day. It is important to highlight that no structural changes have occurred to Better Collective’s equity story; the pressures observed are merely temporary disruptions isolated to “inner-year” growth — a point elaborated in greater detail in section 04. Market & positioning.

Investor sentiment appears to have reset, and the market now seems to be in a “show-me” mode ahead of the Q1-2025 report (May 21). While we expect the upcoming quarter to reflect continued temporary headwinds, our longer-term outlook remains constructive.

After all, the company operates a highly cash-generative model, consistently delivering +70% cash conversion and double-digit adj. ROIC. It holds a leading position across key global betting markets, supported by diversified user acquisition channels, proprietary technology, and long-term media partnerships that provide operating leverage at scale. Further, its revenue base is increasingly becoming recurring-like, which — when paired with the company’s capital-light operating model — provide a clear path to sustained margin expansion.

04. Market & positioning

Online Sports Betting (OSB) remains a structurally growing vertical within the broader global betting landscape, driven by regulatory tailwinds, increasing digital penetration, and a consumer shift toward mobile-first engagement. While the industry is periodically exposed to regulatory friction — particularly during market transitions — the underlying demand has proven remarkably resilient through economic cycles. OSB is largely insulated from broader macro sentiment, supported by its low-ticket, high-frequency, and “entertainment utility” it provides to users. In many markets, betting activity has remained stable or grown during downturns.

Better Collective is exposed to both (i) sportsbooks’ net gaming revenue (NGR); and (ii) their advertising budgets. However, given the company’s strategic shift toward the former, focus will remain on the wider OSB market as a proxy for the underlying market potential.

Three regions stand out as particularly relevant to Better Collective’s growth trajectory and capital allocation focus: Europe, North America (particularly United States), and Latin America (particularly Brazil). Each market sits at a different stage of regulatory development and market maturity, offering distinct profiles in terms of scale, margin potential, and operating complexity.

Still, quality traffic and content remains paramount to capture audience and gain exposure to the revenues generated by sportsbooks. Luckily, operating media sites is more homogeneous across geographies — and Better Collective stands as a clear pure-play leader within this domain:

Europe

Europe remains the most mature OSB market globally, supported by high digital penetration and a well-established regulatory framework. This maturity brings with it a more stable operating environment, including lower competitive intensity around user acquisition. Unlike newer markets, the base of addressable users in Europe is largely saturated, which translates to less aggressive promotional activity (i.e. bonusses) relative to other markets.

To understand the serviceable opportunity for platforms like Better Collective, one must distinguish between gross and net revenue layers. From headline Gross Gaming Revenue (GGR), a series of structural deductions — including gaming taxes, licensing fees, and promotional costs — must be accounted for to arrive at the Net Gaming Revenue (NGR).

Europe has been a “legacy” market for Better Collective, with several local- and regional leadership brands (i.e. Soccernews.nl, etc.). We estimate the European legacy sites drive +120 average monthly visits.

North America

The North American OSB market is in its infancy and scaling rapidly. The U.S. market was effectively non-existent until 2018, when the Supreme Court overturned the Professional and Amateur Sports Protection Act (PASPA), allowing individual states to legalize and regulate sports betting. Since then, the market has expanded rapidly, with over 35 states legalizing OSB in some form and more expected to follow. As such, it is still early in its regulatory and consumer adoption curve, meaning there is a long runway of GGR growth, aggressive operator acquisition spend, and heavy use of performance marketing — making it highly relevant for affiliates and media-led customer acquisition platforms. However, the market remains fragmented across state lines, each with its own tax regime, licensing rules, and advertising frameworks.

The U.S. OSB market has historically leaned heavily on CPA-based monetization, a natural model in the early stages of market formation. However, given the sheer volume of new depositing customers (NDCs) entering the funnel, we view Better Collective’s pivot toward RevShare as a strategically sound decision to maximize long-term value — even if it temporarily suppresses revenue recognition. Capturing lifetime value rather than a one-time acquisition fee introduces meaningful operating leverage as cohorts mature and bet frequency compounds. At the same time, operators are facing intense competition and elevated marketing spend. In that environment, the RevShare model offers a far more aligned and durable value proposition as affiliates are incentivized to deliver high quality-/intent users — hence directly improving operators’ unit economics.

The acquisition of Action Network and Playmaker has put Better Collective in a robust position, driving +50m monthly visits. We expect to see more M&A in the region once the market (and company) has found its footing again.

LATAM

The LATAM region is characterized by low historical regulation (e.g., “grey market”), high mobile penetration, and a deeply ingrained sports culture — particularly around soccer — making it fertile ground for digital betting adoption. Following years of legislative uncertainty, Brazil — the biggest market in the region — passed a regulatory framework for sports betting in 2023, which came into effect on January 1, 2025.

Brazil’s shift to a regulated OSB market now requires users to re-register with licensed operators using national ID. As of February, 35 operators (173 brands) have received licenses — including key Better Collective partners such as Bet365, Betano, and Betfair — though activation dates vary8. While not ideal, we believe the market-scare is overblown. Below are some points of clarification for frequently raised concerns:

What will happen with previously delivered NDCs? Players all have a unique “player-tag”9 enabling continued RevShare capture upon re-registration. Our channel-checks have confirmed this to be the status quo; after all sportsbooks have no incentive to reacquire customers they already own. Having said that, we do believe there will be a loss of accounts (i.e. duplicates flushed out, activation issues, etc.). Further, there is a slight chance of leakage if the player re-registers with a new account that has no overlap/history with the previous account (i.e. different credit-card, phone number, e-mail, etc.). As you will see, we account for this by applying a one-off haircut of 200k Brazilian NDCs in 202510.

What impact will this leave on betting volumes? The betting volumes may be temporarily lower as activity ramps up given not all operators are live yet. After all, the average Brazilian bettor holds ~2.5 accounts (per H2 Gambling Capital). However, with the Brazilian soccer league season having kicked off on March 29, 2025, the blow on GGR is likely cushioned a bit and contained to H1-2025 before recovering.

For Better Collective, this means that RevShare contribution will temporarily impacted (i.e. pushed into the future) — partially offset by higher CPA/CPM/Sponsorship sales given the fierce competition following launch. However, the long term equity story remains intact. Mind you, Better Collective’s traffic is unrivalled in the LATAM market.

Looking more broadly, B2C operators’ body language with respect to Brazil appears relatively constructive — noting that while there is still some friction in the re-onboarding of existing users, the process is manageable, and player engagement remains intact:

So we have seen a few challenges for Brazil due to the changes in the regulatory environment, mainly around some friction in the sign-up process for customers which we've seen impacting activation [BetFair]. (…) The NSX business [incl. Betnacional], (…) is up +20% in Q1 on a year-on-year basis despite some of those regulatory kind of friction challenges.

— Rob Coldrake, CFO at Flutter Entertainment

05. Valuation

Ahead of this section, it’s worth noting that the near-term outlook carries a degree of uncertainty. This stems primarily from limited visibility into both the first- and second-order effects of Brazil’s regulatory transition, as well as player-friendly outcomes during March Madness in the U.S. Hence, while the H1-2025 will likely come out soft on a YoY basis, the longer term equity story remains intact — in fact we believe H2-2025 will already show meaningful sequential progress.

That said, we believe much of this risk is already embedded in both consensus estimates and management’s guidance. Notably, consensus currently sits just above the midpoint of what is a relatively wide guided range. In our view, the guidance appears conservatively framed, consistent with management’s historical pattern of outperforming stated expectations (apart from LY).

Absolute valuation (DCF)

In this section, granularity has been sacrificed for conciseness — yet subscribers may request access to the full model by reaching out on Substack. That said, given the margin-accretive nature of RevShare agreements — a core driver of long-term value — the segment warrants dedicated attention.

Due to limited disclosure around the size and behavior of Better Collective’s RevShare user base, estimating contribution from existing customers requires some inference. We rely on NDC churn assumptions shared at the CMD as a proxy for retention and pair these with ARPU estimates drawn from listed sportsbook operators. While approximate, this framework offers a reasonable basis for modeling recurring revenue from existing cohorts.

We estimate a EUR ~27m revenue headwind stemming from Brazil’s regulatory transition, with the bulk of the impact expected to materialize in H1–2025. We anticipate a material sequential downtick11 in reported figures during the first half of the year, followed by a recovery in H2–2025 as licensed operators ramp up and betting volumes normalize with the closing stages of the domestic soccer season.

To bridge Gross Gaming Revenue (GGR) to Net Gaming Revenue (NGR), we apply weighted deductions for bonuses, taxes, licensing fees, etc. We then apply a RevShare rate of ~23% attributable to Better Collective, resulting in an implied RevShare revenue CAGR of 7.7% through 203112.

On the CPA side, we assume a gradual decline in NDC volume due to the ongoing shift toward RevShare contracts. Revenue per NDC is held flat at EUR 292 (2024-level), implying a -5% CAGR for CPA revenue. Subscriptions are modeled to grow at 2% p.a., and Sponsorships & CPM at 4% p.a. through the forecast period.

Using a WACC of 8.7%, terminal growth rate (TGR) of 2.0%, and return on new invested capital (RONIC) of 12.5%, our DCF implies an upside of +60% to +130%, corresponding to a valuation range of DKK 140–197 per share.

Relative valuation (multiples)

Better Collective currently trades at a forward EV/EBITDA of 9.3x and EV/EBIT of 14.6x (based on consensus) alongside a 10%+ FCF yield. This is despite its proven ability to deliver double-digit organic growth rates and superior unit economics, management actively executing share buybacks, and the OSB markets’ structural tailwinds. For context, its historical average NTM EV/EBITDA is ~12.5x.

The unique business model makes it relatively cumbersome to collect a representative peer group. As such, we include a blended approach (50/50) consisting of both (i) B2C Sports Betting & iGaming; and (ii) B2B Sports Betting & iGaming and Media players with >15% L3Y revenue CAGR.

As it stands, Better Collective trades at a meaningful discount to peers — although we’d argue the company’s (i) superior unit economics; (ii) incremental scale; and (iii) leading market position across key geographies justifies a premium valuation to its peer group. Based on the peer group, implied upside is 50-70% from current levels.

06. Key risks

While we believe Better Collective’s long-term value is materially mispriced, the company remains exposed to a set of “systemic” risks that could impair value realization and cause thesis-drift. Below, we outline five core risks that warrant monitoring:

Regulatory risks: The global trend toward regulation is a net positive for long-term visibility and monetization quality. However, transitions to regulated regimes — as seen in Brazil and previously in the Netherlands — can disrupt existing RevShare cohorts, impose new tax and licensing burdens, or limit user acquisition avenues. In more extreme cases, political or social pressure around responsible gambling could reduce operator GGR, and by extension, RevShare contribution.

Platform and Search Engine Dependency: A meaningful share of Better Collective’s traffic originates via organic search. As such, changes in search engine algorithms, cookie policies, or third-party content restrictions may weaken SEO rankings and result in lower web traffic.

Integration Risk: While Better Collective has a history of successful bolt-on acquisitions, recent deals — notably Playmaker — are larger and structurally more complex.

Event-Driven Volatility: Player-friendly events — such as March Madness 2025 — compress operator GGR and suppress RevShare earnings. Similarly, timing of U.S. state launches, partner marketing budgets, and global sporting calendars introduce quarter-to-quarter variability. While these effects tend to normalize over time, they can distort reported results and cloud underlying trendlines.

Operator consolidation: Better Collective’s business model is structurally linked to the breadth and competitiveness of the online gambling operator landscape. A key driver of favorable RevShare terms has historically been the high level of competition among sportsbooks seeking affiliate-referred customers. However, continued consolidation among operators may reduce pricing tension, weaken negotiating power, and compress RevShare economics over time.

As of April 30, 2025. Prior to this, he was COO

Broken out as a separate segment in Q4-2024. Likely to account for 8-10% of annualized revenue

At IPO, top-1 accounted for ~50% of sales. In 2022 (latest, CMD) top-6 customers accounted for ~60% of sales. We believe top-5 likely accounts for ~50% today

Europe & RoW = ~71% of FY2024A sales; North America = 28.9%

When sportsbooks report 70–80% player retention rates, these figures typically exclude light users or bonus hunters, focusing instead on engaged, repeat customers

I.e. in FY2021A Paid Media accounted for 32.1% of sales and delivered an adj. EBITDA margins of 8%. In FY2024A Paid Media sales accounted for 28.7% of sales but delivered an adj. EBITDA margin of 27.2%.

The company announced an estimated EUR 50m RR cost savings from its cost-reduction program. Back-of-the-envelope calculations suggest that FY2024A adj. OPEX-% (i.e. incl. the EUR 40m RR relief, (EUR 10m already reflected in Q4-2024)) would amount to ~30% of sales.

I.e. Betsson (OM:BETS B) received a license in February but were not in operation until April, as per their Q1-2025 earnings call

Most tier-1 operators (Bet365, Betano, Betfair) use robust CRM systems that link player histories via hashed emails, device fingerprints, or KYC data. These systems are typically designed to preserve continuity of user identity — and thus affiliate attribution — even across sessions or re-registrations

Equivalent to ~14% of estimated total NDCs

I.e. ~30% contraction in Brazilian revenue in Q1-2025, mainly from lower RevShare but partly offset by strong advertising spend amid fierce competition. For context, Flutter reported a -44% sequential decline in revenue for Q1-2025

Average based on channel-checks with people in the industry — mainly from the sportsbooks’ side. Reality is that it varies a lot from one agreement to another, hence the 23% “take-rate” should not be viewed as a fixed figure per se

Avoid annuities at all costs.

Excellent work! Thanks a lot for sharing this. What do you see as (potential) key triggers for the share price in the short term?