EDIT (October 24, 2025): Position closed at avg. sales price of DKK 6.85/share. Last chunk sold on the back of CEO being fired for no apparent reason.

Note: This is a micro-cap stock (MCAP of DKK ~210m) with limited liquidity (ADTV of DKK <1m), which may result in higher volatility, wider spreads, and the risk of moving the price even with small order sizes. Similarly, none of the content constitute investment advice of any kind.

TLDR: Dataproces Group (CPSE:DATA) is a Denmark-based GovTech micro-cap offering consultancy and SaaS solutions to local governments in Denmark. Its core value proposition lies in optimizing municipalities’ financial management by reclaiming lost revenue, improving budgeting accuracy, and automating manual workflows.

Following a rough start to the public markets, new leadership has restored momentum — near-doubling ARR L2Y, lifting cash EBITDA margins to ~30%, and >100% cash conversion. With penetration of 90/98 municipalities and significant white space (4–5x ARR potential from upselling alone), plus latent pricing power yet to be exercised, the current price (DKK 6.18/share) offers an opportunity to own a sticky, non-cyclical, asset-light business growing at double digits at ~12x fwd EV/cash EBITDA with ~80% upside on conservative assumptions — fully discounting likely TAM expansion (new products, expansion).

Near term catalysts include expansion to Germany-/Sweden, though risks of churn amid competition from KL-owned (Local Government Denmark, nonprofit) should be monitored closely.

Background

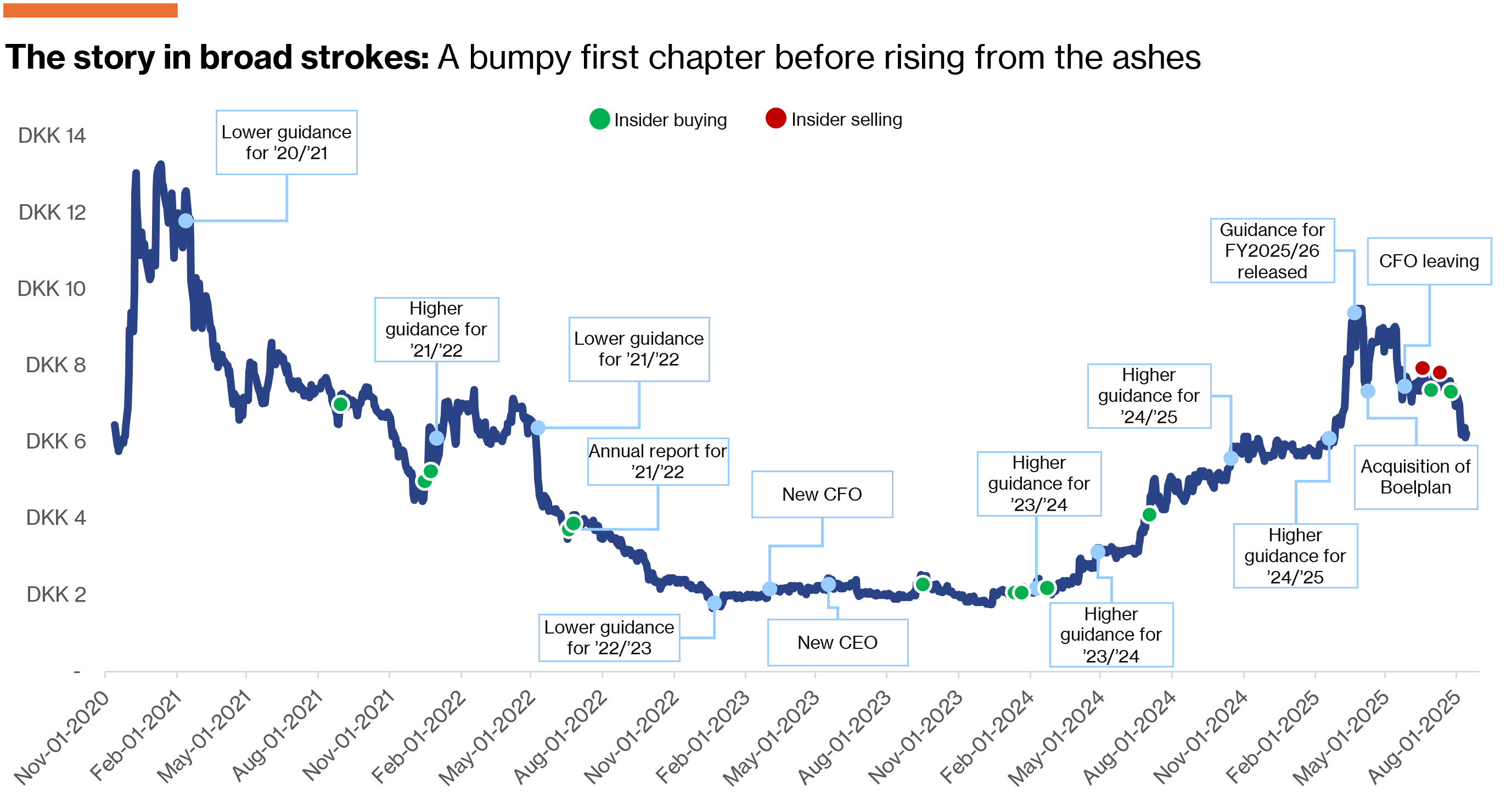

The company listed on Nasdaq First North in late 2020 at DKK 5.00/share (equiv. to MCAP at DKK 152m). While the IPO was oversubscribed 1.6x, the company quickly ran into problems as demand for consultancy services during the 2nd wave of lockdowns waned — though the company reassured investors that projects were “delayed, not cancelled”. Management’s somewhat confusing communication, particularly in the context of guidance revisions, were not exactly helpful to restore investor confidence. Nor was it helpful that the otherwise “scalable” platform could not seem to budge the trend of negative profitability.

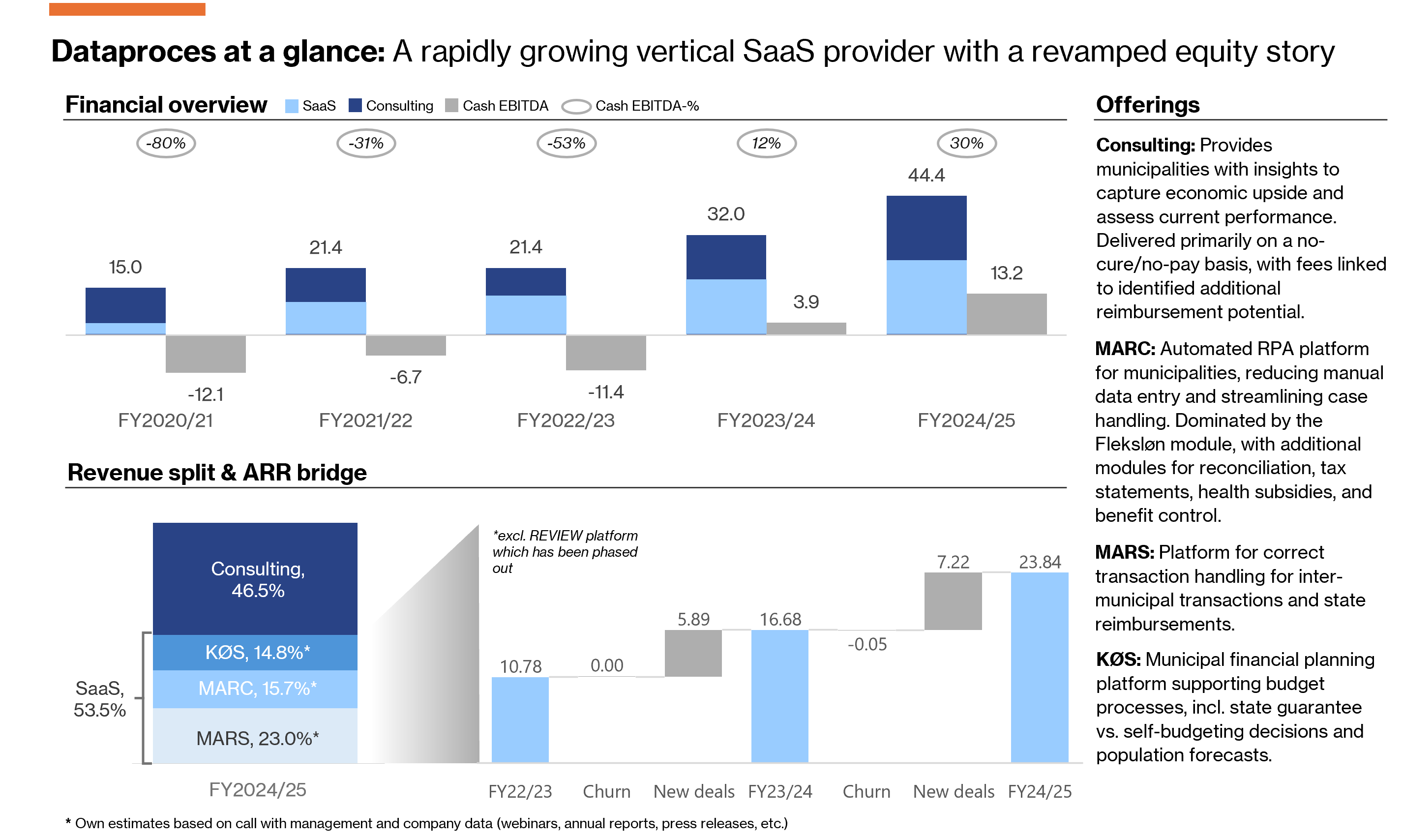

In mid-2023, the company’s founder and CEO, Kjartan Jensen1 finally opened the door for a new leadership team, and passed the torch to Michael Binderup. A few months into his role, he had debt-providers2 (bridge-financing) convert their debt to equity to restore its urgent need for liquidity (~9% dilution), and start from scratch. Since then, it appears the company has found its footing with a right-sized organization (1/5 headcount reduction) while landing contracts with new municipalities and upselling to existing ones. The efforts are mirrored in financials L2Y with ARR more than doubling (granted, from a low base), cash EBITDA margins going from negative to ~30% and a +100% cash conversion.

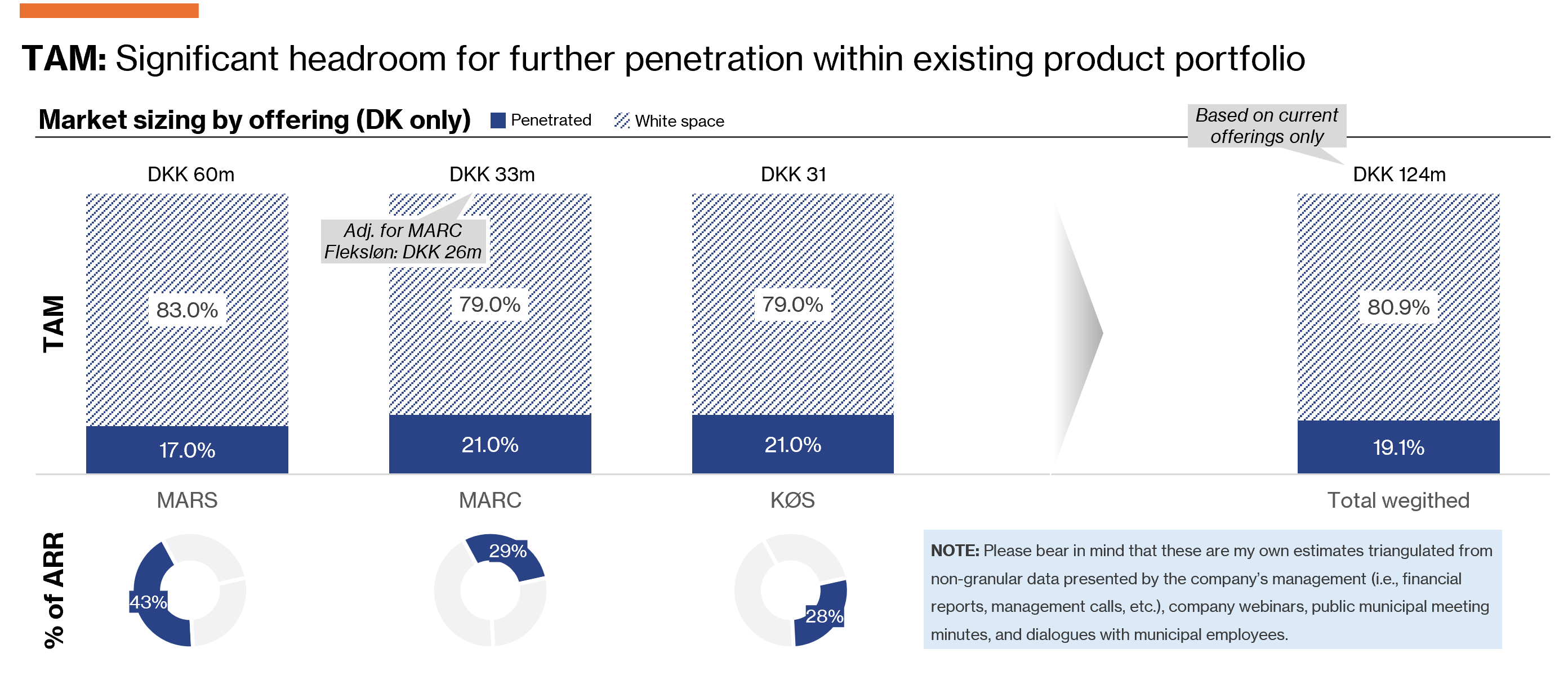

While shares have had a nice run from its low-point of DKK ~2/share, I believe there is additional upside ahead. The customer list currently counts 90/98 municipalities (which exhibit strong loyalty3), yet SoW growth potential is material — according to my estimates, there is white space equal to 4-5x ARR solely from upselling (i.e., excl. new launches and international expansion). As for expanding abroad, the company recently announced its acquisition of Boelplan, a provider of population forecasting, among other, to municipalities in Denmark (17) and Germany (6). Provided Dataproces can leverage this “foot-in-the-door” in Germany, the upside in the years ahead could be material — though it is admittedly easier said than done.

Business model & industry dynamics

To fully grasp Dataproces’ value proposition, it helps to first understand the structure of the Danish public sector — particularly the interplay between the 98 municipalities and the central government.

Local autonomy, central oversight

Denmark is a highly decentralized welfare state where (i) the government handles oversight and financing4, and (ii) municipalities are tasked with execution — delivering services, collecting data, and managing a complex array of welfare reimbursements. This relationship creates friction by design — but it is also what drives the financial incentives that Dataproces seeks to “arbitrage”. With complex (and constantly evolving) laws and continued pressure on public budgets, minor errors in case handling can compound into significant financial misallocations.

Dataproces’ value proposition essentially allows municipalities to unlock lost revenue (i.e., reclaim misallocated funds), optimize financial planning (i.e., population forecasting), and reduce administrative burden by automating error-prone workflows.

Example of value prop (translated): The pilot project [with Dataproces] is now complete, and has yielded annual net gains of DKK 3.5 million related to the subsidy- and equalisation system. This is a significantly better outcome than initially expected (…). It has therefore been decided that the gains from the completed pilot project will be allocated to a reserve, earmarked to cover costs necessary for further digital revenue optimization.

— Aarhus Municipality, Budget reserves 2017

Layer on top of this the mismatch between the central government's “state-of-the-art” tech suite and the municipalities’ fragmented, often outdated digital infrastructure. Yes, Denmark is widely regarded as a front-runner in public-sector digitization — but that status masks an internal imbalance as sophistication of digital capabilities varies widely across the municipal landscape. With the government now aiming to position Denmark at the forefront of AI adoption in the public domain, the need for municipal catch-up is long overdue.

Pure-play enabler of municipal revenue-/cost optimization

Dataproces’ operations are divided into two main segments:

Consulting (44% of FY24/25A sales): In this segment, the company provides consultancy services (“data analysis”) for municipalities, aiming to uncover lost revenue across a wide range of domains (i.e. VAT reimbursements, state equalisation transfers, social benefits (e.g. disability, housing), inter-municipal settlements, etc.). All projects are based on a “no cure, no pay” basis5 — suggesting that, although the municipalities have employees to “kick the tires”, Dataproces is almost certain to find something. These projects also serves as an entry point for new SaaS sales as the credibility gained through successful consulting engagements frequently leads to subsequent SaaS contract, enabling municipalities to capture the identified savings on a recurring, run-rate basis. Similarly, the consulting/data analyses also enable Dataproces to discover other inefficiencies for which new software modules can be developed. On the flip-side, the consulting segment offers limited financial visibility — both due to the lumpy nature of project timing and, more importantly, the lack of upfront clarity around final revenue realization.

SaaS (54%): Dataproces currently operates with three6 platforms, offered on an annual subscription. Each platform comes with different modules for various use-cases:

MARS: The MARS platform is built to help Danish municipalities navigate the complexity of intergovernmental funding by ensuring the municipality gets what it is owed. It essentially automates and validates the countless micro-transactions that occur between municipalities and the state (i.e., reimbursement claims, residency tracking, VAT handling, etc.)

MARC: The MARC platform is aimed at automating manual labor across a host of repetitive tasks in respect to calculating, auditing, and reconciling public aid.

KØS: The KØS platform essentially gives municipalities the ability to use its data to anticipate shifts in both their income and expenditure — so as to accurately budget ahead. This is done by mapping population trends, age shifts, and its projected cost drivers as well as track how key revenue streams (grants, tax transfers, reimbursements, etc.) are developing over time.

Unfortunately, the company does not provide revenue split across solutions for “competitive reasons”. Hence, I have estimated the sales split by way of triangulating public data — incl. contract wins, pricing7, municipal meeting minutes, management commentary, etc. — with my own DD from speaking to management and municipal employees. Based on my estimates, the MARS platform is the largest (~43% of FY2024/25A ARR), followed by MARC (~29%) and KØS (~28%).

Customers are billed on a module basis (i.e. each platform comes with x number of modules for which the municipality can (de)select according to their needs). In that context, a sales split across modules vis-á-vis platforms is perhaps more important — and while management is tight-lipped on this matter, they have added a bit of nuance. Its MARC Fleksløn module, which is currently facing competition from KOMBIT (more on this in the next section), accounts for a big chunk (~19%) of total AAR.

The reason each module come with a separate agreement is to keep the total offering below the thresholds for contracts that are subject to a compulsory call for tender (DKK 1.6m). This makes the decision process faster and less bureaucratic. On the flipside, it also means that contracts are subject to “annual review” as opposed to, say, 4-5 year contracts — though comfort is taken in the low churn rate historically. The contracts run with 3 months termination to the end of the calendar year, and include annual price revision according to the anticipated development in the salary- and price index provided by municipalities' national association (“Kommunernes Landsforening”). Most recent datapoints point to 3.1% for 2025/26.

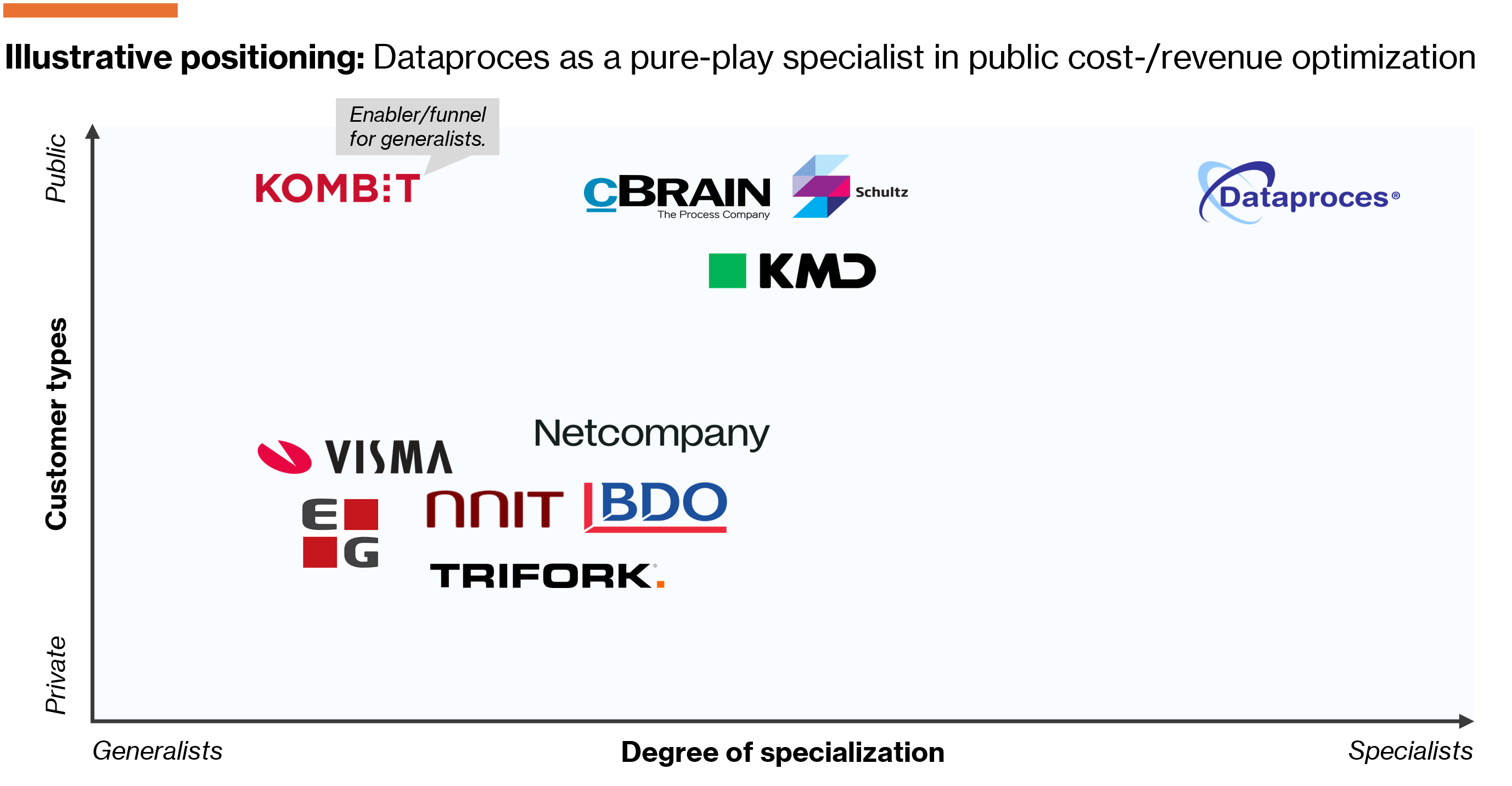

Competition

The landscape for digital workflow solutions within niche municipal workflows (i.e., revenue- and cost optimization) is fragmented and still in a relatively early phase of adoption. In that context, the closest competitor is often the municipalities themselves relying on manual processes, in-house spreadsheets, or siloed legacy systems to manage complex financial tasks. Having said that, there are a few players seeking to capitalize on the latent market potential, consisting of a mix of larger generalists and a tail of smaller players.

While it’s difficult to isolate direct overlaps in functionality, I believe the most credible set of peers are:

KMD which was previously owned by KL — the Danish municipalities’ association — before being sold in an LBO to EQT and ATP in 20088. The company is by far the largest IT provider to municipalities, aided by its monopoly-like start as a private company, though competition has intensified. My discussions with management and employees across four municipalities suggest that Dataproces has taken share from both over the past years.

KOMBIT is basically KMDs successor; a non-profit municipally owned IT community (100 % owned by KL) with the caveat that they do not develop software themselves. Instead, KOMBIT acts as a strategic aggregator by leading tenders, managing shared IT infrastructure, and overseeing roll-out of platforms. One of its key offerings is Kommunernes Ydelsessystem (KY), a national case-processing platform to which new functionalities are added on an ongoing basis.

Across the board, users highlight Dataproces’ domain expertise and high-touch relationship — attributes often lacking in large-/generalized providers. One particularly telling example: Dataproces manages a Microsoft Teams group (“ERFA”) that facilitates ongoing knowledge-sharing among municipalities. Should Dataproces continue to scale successfully, I could see KMD, BDO, EG, or Visma emerge as a strategic acquirer.

In my view, KOMBIT represents the most credible threat to Dataproces — underscored by the recent mandate given to Netcompany (CPSE:NETC) to develop "FLT", a direct competitor to Dataproces’ MARC Fleksløn. User testing for FLT began in June 2025, with formal roll-out scheduled for Q4-2025/Q1-2026. Dataproces management has been upfront about the risks (churn) as a result of this, as reflected in their cautious FY2025/26 guidance — elaborated in the next section.