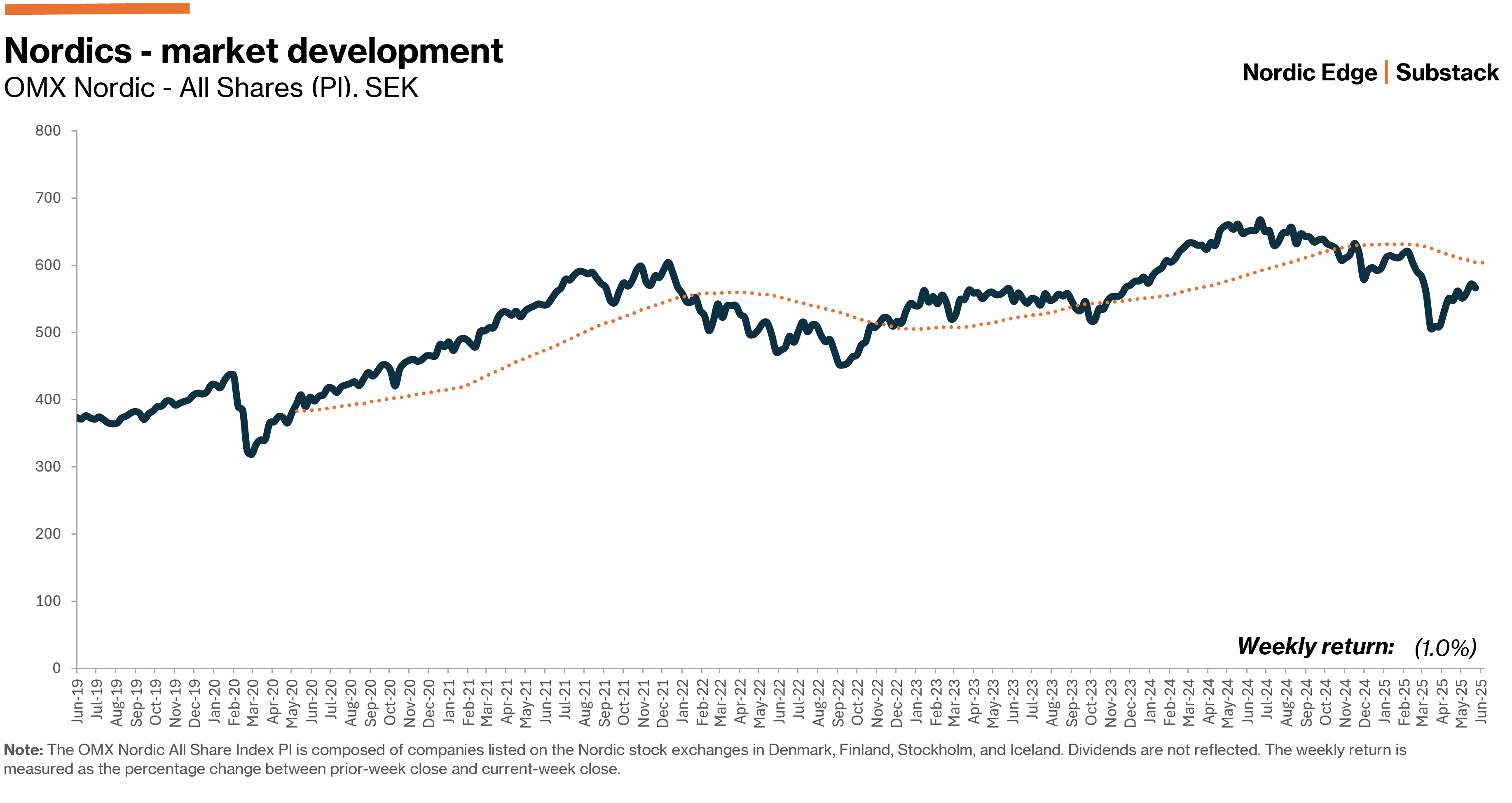

Monday Morning Espresso W24'25

Markets navigated a tense macro-political backdrop last week. Early in the week, signs of progress in U.S.–China tariff talks offered some relief, though the endgame remains unclear. U.S. inflation data surprised to the downside, increasing pressure on Fed Chair Powell to cut rates; the market currently expects two rate cuts (September, December) for 2025. Toward week’s end, Israel’s strike on Iran escalated the conflict in the Middle East, sending commodity prices higher and airline-/travel stocks lower.

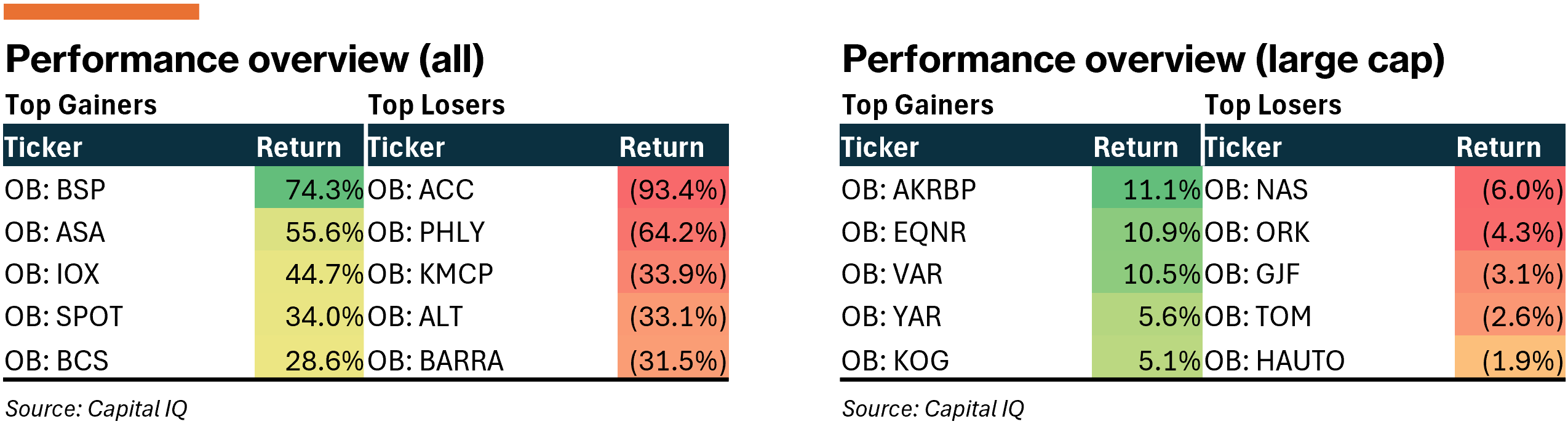

The Nordic markets ended the week slightly down (-1.0%), though with notable divergence across countries. Norway closed at all-time highs and Denmark continued its catch-up to the wider region, while Sweden and Finland took a breather. The week also saw two new IPOs: mortgage lender Enity (OM:ENITY) in Stockholm and construction firm Sentia (OB:SNTIA) in Oslo — both drawing strong investor interest.

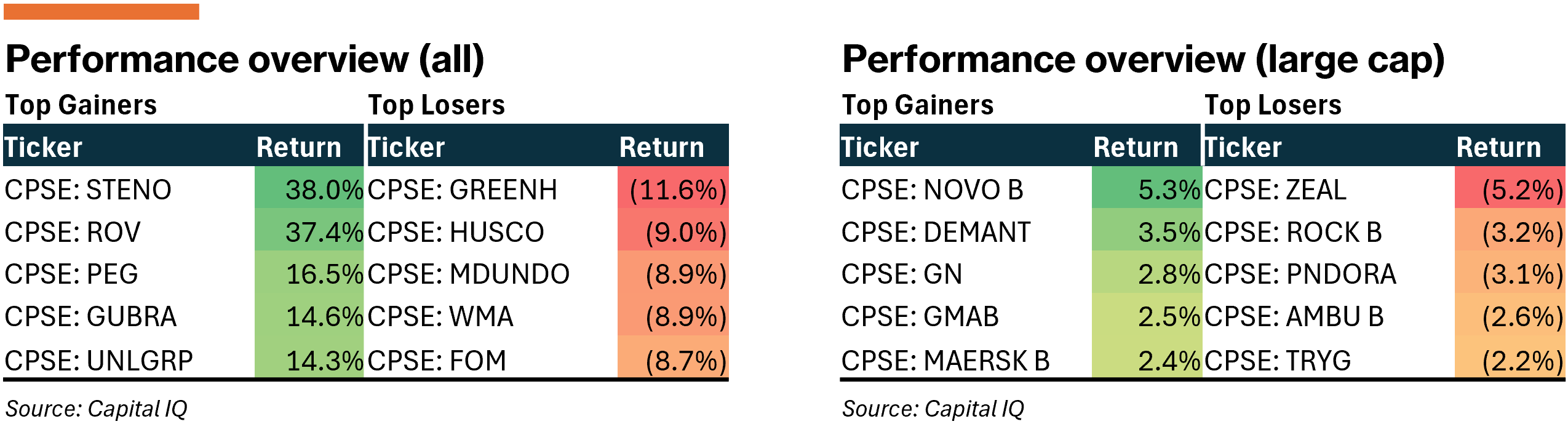

Denmark

Last week’s spotlight fell on Novo Nordisk (CPSE:NOVO B) following reports that activist hedge fund, Parvus Asset Management, is building a stake. Similarly, Demant (CPSE:DEMANT) gained traction after announcing its largest acquisition to date. Meanwhile, concerns re-emerged around HusCompagniet’s (CPSE:HUSCO) operational robustness following media reports about quality issues.

In aggregate, shares in Denmark escaped the week unscathed, with the all-share (+2.1%) and large cap (+0.3%) indices ending the week in green.

Relevant news:

The London-based hedge fund, Parvus, is reportedly building a stake in Novo Nordisk (CPSE:NOVO B) with the aim of influencing the CEO succession, following Lars Fruergaard Jørgensen’s departure. While the company’s share and voting structure renders activist influence unlikely, the move may reflect a contrarian bet on valuation normalization after a sharp pullback in the past 12 months.

Demant (CPSE:DEMANT) announced the EUR 700m (DKK 5.2bn) acquisition of Germany’s Kind Group, a retail hearing care chain with ~650 clinics across several countries. The deal expands Demant’s footprint in Europe’s largest hearing aid market and is expected to add EUR 300m (DKK 2.2bn) in revenues by 2026. The transaction implies an EV/Sales (2025E) multiple of ~2.7x, and will be 100% debt-funded.

HusCompagniet (CPSE:HUSCO) shares fell after media reports exposed quality issues (crumbling mortar joints) in delivered homes. The company has taken legal action against mortar supplier Dan-Grit, though full visibility on accountability remains unclear. We fear that there may be structural project management challenges, potentially exacerbated by recent large turnkey project commitments.

The hedge fund, Marshall Wace, has reportedly reduced its short position in GN Store Nord (CPSE:GN). According to Bloomberg, the fund cut its position by DKK 1.3m (0.86% of share capital), leaving a remaining short equivalent to 7.5% of shares outstanding.

Novo Nordisk (CPSE:NOVO B) announced that its next-generation weight-loss candidate, amycretin, is headed into Phase 3 trials. The molecule combines GLP-1 and amylin in a single structure — potentially simplifying treatment and easing oral formulation and scalability.

Bavarian Nordic (CPSE:BAVA) has initiated a Phase 3 trial of its single-dose chikungunya vaccine, VIMKUNYA, in children aged 2–11. The study seeks to expand the current label, which covers individuals 12+ and is already approved in the US, EU, and UK. Primary results are expected in H1 2028.

Ørsted (CPSE:ORSTED) is reportedly preparing to divest a portfolio of 27 onshore wind assets across Ireland, England, Germany, and Spain, totaling ~800 MW in capacity, per PeakLoad. Non-binding offers are expected in July, with the portfolio potentially valued up to EUR 2bn. The move follows earlier reports of financial strain and aligns with Ørsted’s broader efforts to streamline its asset base.

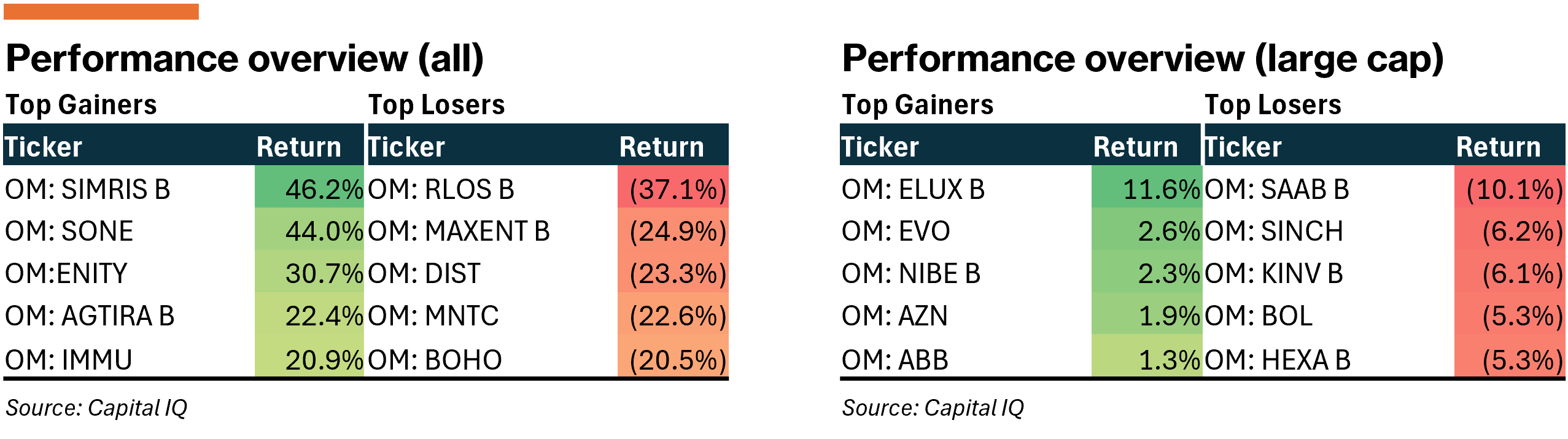

Sweden

A relatively calm week in Stockholm, marked by large block trades involving cornerstone investors and a handful of M&A/IPO headlines. Defense stocks came under broad pressure after Deutsche Bank downgraded its view of the European defense sector. The all-share (-1.6%) and large-cap (-1.5%) ended the week down as recent gainers gave back gains.

Relevant news:

CVC Capital last completed its full exit from Synsam (OM:SYNSAM), selling its remaining ~16.5% stake at SEK 46/share — a 4.3% discount to the day-prior close. The move is consistent with our call in week 11, when we flagged that CVC was likely to fully exit its position within 6–12 months following its initial block sale. The transaction has effectively removed the overhang tied to sponsor selling.

Enity (OM:ENITY), the specialist mortgage lender behind Bluestep and 60plusbanken, made its debut on Nasdaq Stockholm on Friday. The IPO — an all-secondary sale by EQT via Butterfly Holdco — was heavily oversubscribed, with demand exceeding supply by over 10x. Priced at SEK 57/share, the stock closed ~31% higher by close on its first day of trading.

SAAB (OM:SAAB B) traded gave back gains following Deutsche Bank’s downgrade of the European defense sector — amplified further by downgrades from BofA and SEB, both pointing to stretched valuation as the company trades at a ~30% premium to peers.

Take-private rumors around H&M (OM:HM B) persist — despite repeated public denials — as the Persson family continues to build its stake, now holding 70% of capital and ~85% of voting rights. Sentiment weakened further last week after peer, Inditex (BME:ITX), missed expectations for Q1-2025/26 sales and early summer trading.

EQT and Fortnox chairman Olof Hallrup, via First Kraft, are pressing ahead with their offer for Fortnox (OM:FNOX) despite falling short of the 90% threshold required for a squeeze-out. The consortium now controls 80.5% of shares and has extended the acceptance period to June 25.

Clas Ohlson (OM:CLAS B) delivered another solid quarter in Q4 2024/25, with total sales rising 8% YoY to SEK 2,343m (vs. SEK 2,280m cons. | SEK 2,167m LY) and online revenue up 19% to SEK 493m. EBIT landed at SEK 109m (vs. SEK 92.1m cons. | SEK 65m LY). The strong momentum has supported a dividend hike to SEK 7/share (vs. SEK 4.25 LY) and management reaffirmed its plan to open ~10 new stores (net) in FY 2025/26.

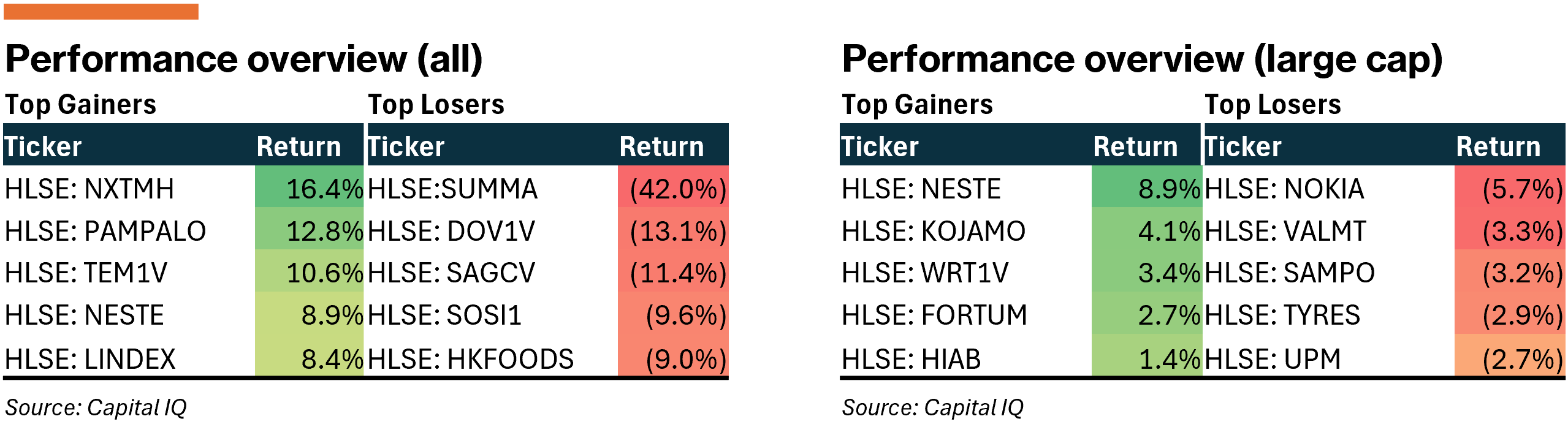

Finland

News flow out of Finland was relatively more busy vis-à-vis the previous weeks, yet materiality was relatively benign. The all-share (-1.1%) and large-cap (-1.0%) ended the week slightly down.

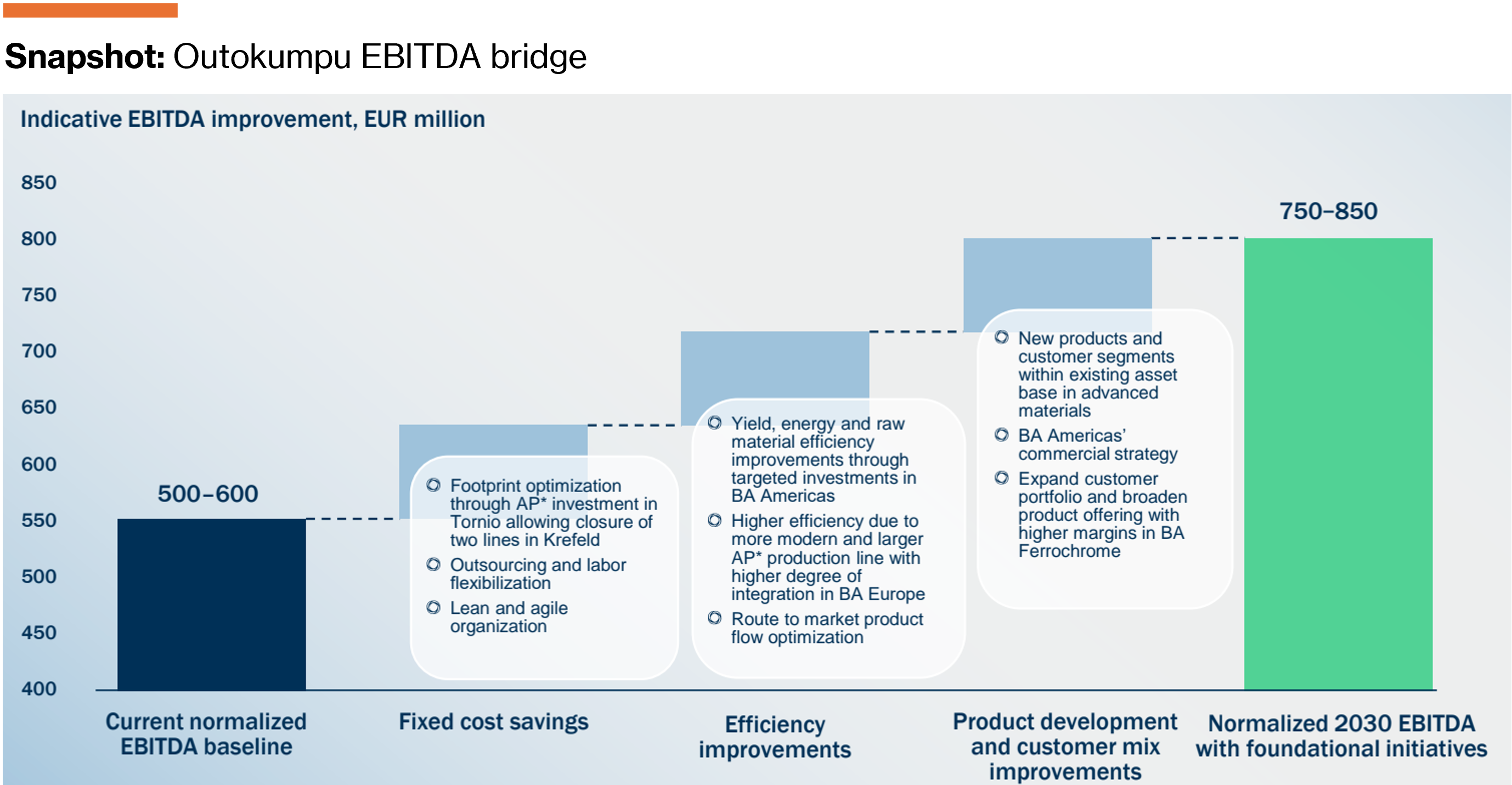

Outokumpu (HLSE:OUT1V) hosted its 2025 Capital Markets Day, introducing its new “EVOLVE” strategy for 2026–2030. Management communicated two IRR thresholds for investment: >15% for “Foundational” projects (stainless and ferrochrome) and >20% for “Transformational” initiatives (e.g., high-nickel alloys, high-chromium content). As part of the strategy, management disclosed a EUR 200m growth capex commitment to build a new annealing and pickling (AP) line at Tornio, Finland — expected to replace capacity closed in Germany — and reiterated a EUR ~600m maintenance capex across the period. Combined with product mix upgrades and cost-out measures, normalized EBITDA is targeted at EUR 750–850m by 2030.

Management also flagged potential M&A but set clear balance sheet guardrails (ND/EBITDA ≤2.0x, target 1.0x), with total capex capped near EUR 1bn for the period. Dividend guidance was not formally expressed — we believe it is fair to assume it will stat flat. The shares currently trade at ~5x EV/EBITDA (FY26), thus we see limited upside without visible delivery on growth targets.

Relevant news:

Kojamo (HLSE:KOJAMO) has announced the sale of a portfolio of rental properties to funds managed by Apollo and Avant Capital Partners. While key financial terms were not disclosed, the transaction supports Kojamo’s strategy to streamline its property holdings and improve capital efficiency.

Tecnotree (HLSE:TEM1V) announced a five-year agreement with an unnamed global mobile virtual network operator to deploy its digital Business Support System platform in the UK and other European markets. The contract is valued at USD ~50m, with initial revenues expected in H2-2025.

Lassila & Tikanoja (HLSE:LAT1V) announced progress on its planned partial demerger, aiming to separate its circular economy operations into a new listed entity. As part of the process, the board has proposed appointing Eero Hautaniemi as CEO of the circular economy business and Antti Niitynpää as CEO of property services.

Lindex (HLSE:LINDEX) has reached a settlement with Lähi Tapiola regarding the final dispute in its restructuring program, tied to lease termination compensation for its Tapiola department store. The undisclosed settlement clears the last major liability classified as restructuring debt and allows the company to apply for early termination of the program.

Fiskars (HLSE:FSKRS) issued a profit warning, cutting its 2025 adj. EBIT guidance to EUR 90–110m (vs. prior guidance for improvement from EUR 111.4m in 2024). The downgrade follows a sharper-than-expected drop in U.S. demand in Q2-2025, driven by the indirect effects of import tariffs on retail sales and inventory levels.

Meriaura Group has completed its acquisition of Summa Defence in a reverse listing valued at EUR 187.7m, implying a 2024 EV/Sales multiple of 3.8x. As part of the deal, Meriaura issued 4bn new shares to Summa shareholders, significantly diluting existing ownership. Shares now trade under the ticker code SUMMA.

Scanfil (HLSE:SCANFL) announced the acquisition of 80% of ADCO Circuits Inc., a Michigan-based contract electronics manufacturer, for EUR 13.6m, valuing the business at EUR 21.7m (EV, 100%). The deal excludes ADCO’s facility and is expected to close in Q3-2025. The move boosts the company’s U.S. footprint, particularly within aerospace and defense, which represents 37% of ADCO’s sales.

Norway

Momentum in Norway persisted last week, with equities reaching new all-time highs and extending their outperformance relative to Nordic peers. The advance was largely driven by oil producers and tanker companies, benefiting from rising crude prices amid renewed Middle East tensions. The week also featured the anticipated IPO of construction group Sentia (OB:SNTIA), which was ~15x oversubscribed and closed up 14% on its trading debut.

The all-share index rose +3.4% and the large-cap index +3.0%, primarily driven by broad gains in index heavyweights as commodity prices strengthened toward the end of the week.

Relevant news:

Sentia (OB:SNTIA) successfully completed its IPO on the Oslo Stock Exchange, pricing shares at NOK 50 and implying a market cap of NOK ~5bn. The offering raised NOK ~1.6bn and was ~15x oversubscribed. Shares closed up 14% on the first day of trading.

SoftwareOne (SWX:SWON) will complete its acquisition of Crayon Group (OB:CRAYN) with settlement expected to occur at 2 July 2025. Shareholders will receive NOK 69 in cash and 0.8233 new SoftwareOne shares per Crayon share. The deal, initially announced in Dec-24, implies an EV of NOK ~16.8bn and an EV/EBITDA (Q3-2024 LTM) of 18x. Delisting from Euronext Oslo is expected to follow.

Bluenord (OB:BNOR) has successfully completed a 30-day production test at the Tyra gas field, satisfying key requirements for field completion. The milestone clears the path for the long-delayed field to move into full operational status. With this hurdle passed, Bluenord expects to declare a dividend of USD 253m (NOK ~2.55bn) to its owners in the near term, equivalent to a 15% dividend yield.

Telenor (OB:TEL) is reportedly exploring a potential acquisition of 3 Scandinavia. The move is said to be motivated by more favorable EU signals toward telecom consolidation, and would mark a strategic step for Telenor in strengthening its Nordic footprint. 3 Scandinavia is Sweden’s fourth-largest mobile operator and generated 2023 revenues of SEK 12.5bn and EBITDA of SEK 3.5bn.

Orkla (OB:ORK) is preparing for an IPO of its Indian subsidiary, Orkla India Ltd, with plans to sell 22.8m shares, incl. 20.6m from majority owner Orkla Asia Pacific Pte. Ltd. According to Bloomberg, Orkla is targeting a valuation of USD ~2bn and initially aimed to raise up to USD 400m in fresh capital. The listing is set to take place in Mumbai.

Zalaris (OB:ZAL) concluded its strategic review and will continue executing its current strategy. Management noted that while the company had received several acquisition offers, yet none of them were believed to have a premium that adequately reflects Zalaris’ value. We hope for more color on the matter in due course.

Akva Group (OB:AKVA) held its capital markets day on Thursday, setting new long-term financial targets. The company aims to reach NOK 5bn in revenue by 2027 and NOK 7bn by 2030, up from NOK 3.5bn in 2024 and an expected NOK 4bn in 2025. Management emphasized the need for technological investment across the salmon industry to reignite growth after several years of production stagnation.